Rates fears and market volatility

Markets have been volatile as fears of rising interest rates are leading to valuation changes in bond and equity markets – US 10 year Treasuries jumped from from 1.08% to 1.52% in February. Serious thinkers including Lael Brainard (a Governor of the Federal Reserve in the US) was reported in the Wall St Journal as follows: “I am paying close attention to market developments. Some of those moves last week and the speed of the moves caught my eye. The economy remains far from our goals in terms of both employment and inflation, and it will take some time to achieve substantial further progress. We will need to be patient to achieve the outcomes set out in our guidance.”

We are inclined to believe her, with respect to the official position. But, in our view, central banks’ actions are dictated by the economy (not the other way around); the increasing bond yields are suggesting that the market is not in agreement with the official view and has expectations of rising inflation and interest rates.

Predictably, markets sold off, including a number of holdings in the Loftus Peak Global Disruption Fund. In the recent months, we observed overvaluation in some pockets in the market and accordingly maintained a high cash exposure, to be redeployed once we are comfortable with particular company valuations. We still see a number of businesses with valuations that don’t make sense. For example, Shopify (which we don’t own), a very fast-growing company which creates a web presence as a service to small (or large) merchants is currently capitalised at around US$200 billion. It is true that the company also provides back-end services such as web design, the payment engine and even some accounting functions, but does that make it worth 50% of the value of Visa, Walmart or JP Morgan?

Which brings us to the real point of today’s comment – risk-adjusted returns.

Loftus Peak’s portfolio construction methodology and risk

Which is the better investment, a company that goes up 10x, but has a chance to go broke, or a company that has a higher probability of rising 50-60% with a downside of 20%? That of course depends in part on an individual’s risk tolerance, which is tied up with the appetite for risk/non-risk assets. However, for the Loftus Peak Global Disruption Fund, we believe the answer is the latter. We are acutely aware that the monies we invest are mostly those belonging to others, and that we have a duty to treat our investors’ money as we would our own. Our portfolio construction process is no different to that of the reasonable investor managing a personal position – higher allocation to assets with a high probability of achieving the target returns and a lower allocation to “moon shots”.

All of this goes to the risk and reward profile of the individual companies we own. We don’t allocate substantial funds to the companies with the greatest upside, rather we allocate funds based on our assessment of the risk-adjusted upside for the portfolio. It therefore follows that our largest positions are in companies with a greater certainty (lower risk) of achieving our modelled cashflow targets. Most of the companies which fall into this category are those that are well run, highly cash generative, with large capitalisations and strong balance sheets – this forms the “core” of the portfolio. These companies do not require multiple years of hypergrowth (which have inherently higher execution risk) to justify valuations. A smaller allocation is made to companies that are emerging as strategic players in a thematic and have higher growth prospects, but which have a relatively lower certainty (higher risk) of achieving modelled cashflow targets – these might be smaller or less financially sound companies and are “non-core” positions. We have observed that this intentional tilt towards “core” positions provides the bedrock for strong portfolio returns (by capturing risk-adjusted upside) and protection during times of volatility.

Managing risk as a path to return

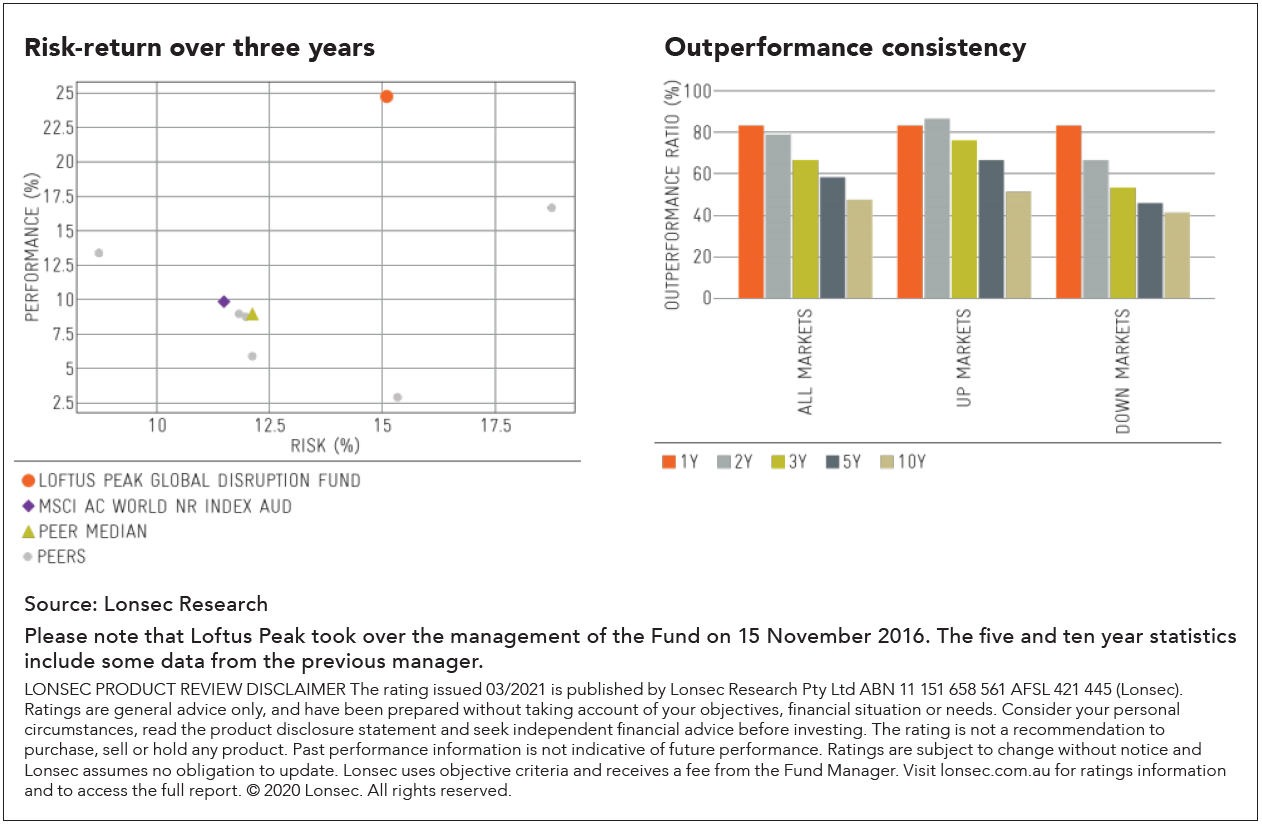

We are often perplexed when some market commentators talk of risk and return as if they were mutually exclusive. In our opinion, no one should make a decision based on one of these factors alone – the question always should be how much risk the portfolio was exposed to in order to generate the returns. Fortunately, there are various simple statistical ratios which one can use to standardise the risk and return across different portfolios. Two such measures, extracted from the Lonsec’s product review of the Fund are shown below.

The first chart shows that Loftus Peak has generated significantly higher returns for a small increase in risk (volatility) relative to the peer median over three years. This is confirmed in statistics provided by Lonsec referring to the information ratio of 1.55 compared with peer median of -0.16 (higher is better). The information ratio measures the consistency with which a fund manager generates excess returns. Readers can learn more about information ratios here.

The second chart above shows Loftus Peak has high outperformance consistency in down and up markets over one, two, three and five years. This is our fifth year of managing the Fund – so technically the five year number isn’t entirely ours (which is actually better).

Notwithstanding, outperformance in all markets, both down and up, is only possible if risk is adequately considered and controlled. We appreciate this can mean that we give up some short term performance, for this, but the mix between risk and reward has served investors well over the seven years we have been managing client monies.

We highlight these risk metrics because we actively manage to them, and of course note that past performance does not constitute a guarantee for the future.

We believe that the solid investment returns over time of the Loftus Peak Global Disruption Fund are a result of sensible stock selection, in our case driven by the powerful disruption thematic that is impacting all industries, and portfolio construction that respects valuation risk.

Share this Post