A doctored photo of Xi Jinping in a flying car has been circulated on-line. The picture is fake, but the flying car isn’t – see the one above, a version of which was at the Melbourne Electric SUV Expo in 2025.

It is actually an X-Peng two seater drone, powered by at least eight electric rotors. It can be piloted onboard, with the possibility that it may also be operated remotely.

(Side note: we first saw a version of the flying X-Peng at a Shanghai car show five-ish years ago. It was effectively a very large drone with enough battery-powered motors to carry one or two people. Its existence raised more questions than it answered, like how it would work traffic-wise in the event of significant uptake, and how it performed in poor weather such as high winds. Setting these questions aside, it was an obvious – drones had been around for years even then – but nonetheless startling development. The implications were and are significant.)

As interesting as the flying car is, it is a long way from commercial reality. What is here right now is the pace of growth of the Chinese electric and hybrid car industry.

China already largest hybrid/electric car player

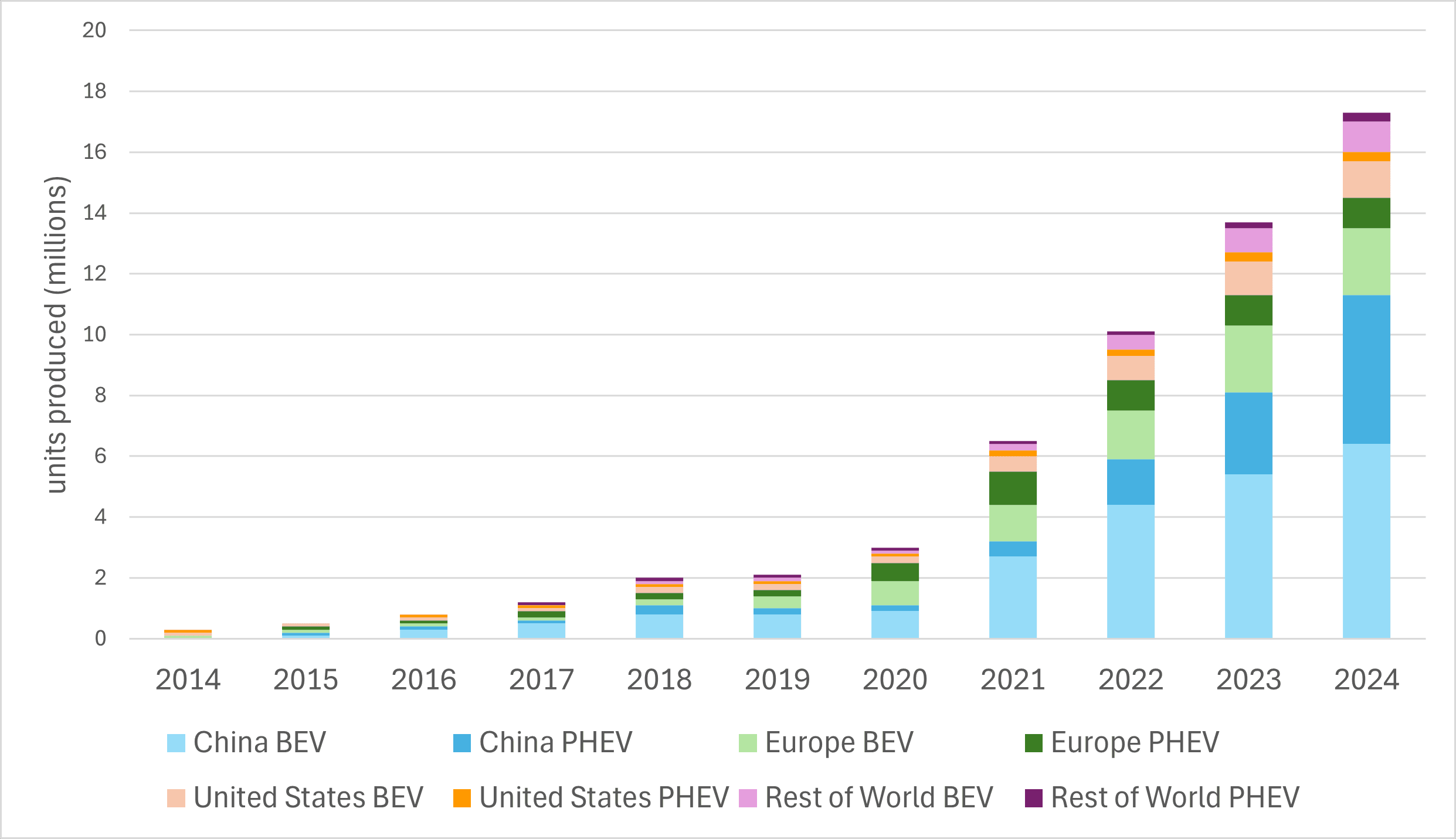

The chart below shows global electric car sales, with light and dark blue bars representing China’s production of electric and hybrid vehicles. The important thing to note is that it now stands at over ten million units, from around only one million in 2020.

Source: International Energy Agency

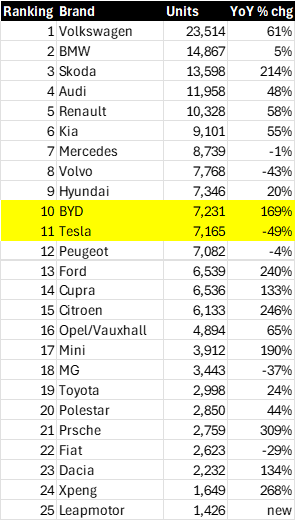

BYD registrations exceeded Tesla in Europe

The largest of those Chinese car makers, BYD eclipsed Tesla in European EV car registrations in April 2025, growing +169% YoY to sell 7231 units while Tesla sales actually fell -49% YoY, with fewer cars sold outright (7165) than BYD in that period, as the table below shows.

Most registered BEV brands April 2025 Europe

Source: JATO

BYD now the third largest car company by market value

The top three car companies by value in the world today are Tesla, which has a market capitalisation of just over US$1 trillion, with Toyota second at US$221 billion and BYD third at US$140 billion. Relative to the numbers of cars produced, Toyota is ranked number one compared with VW group, a reversal from just a few years ago.

But when considering the market value of car companies, some further explanation is required. In our estimation, around 20% of Tesla’s current market value is related to car production (this is a view broadly shared across the market). The rest of the value is robotaxis, home power and robotics, especially Optimus. But the valuations of BYD and Toyota, as well as other Japanese and European companies reflect a deep shift in how investors view Chinese car makers.

Source: BYD

Japanese car makers and to a lesser extent Europeans dropped the ball with EV’s.

In the case of Toyota, the company continues a lead it began in hybrid cars. These cars found popular uptake at the lower to mid end of the market. Separately, Toyota spent decades researching hydrogen-based transport. They even launched a poorly received hydrogen car, the Mirai, sales for which were just 1,778 in 2024 (down -56% year-over-year).

Hydrogen has not found significant uptake because of lack of fuel infrastructure. It is not a fuel which liquefies easily. By way of further evidence of the questionable future of hydrogen, just in the past weeks Australia’s Andrew Forrest has announced the closure of two hydrogen plants, one in the US and one in Queensland. Thinking this through across the decade, Toyota has arguably lost the high ground by putting too much time and energy into hydrogen, work that has not yielded good results.

Back to our trips to Shanghai, the first of which was more than ten years ago. The cars on offer at that and subsequent technology fairs were very poorly thought-out, crude attempts at EV production. They remained that way for some five years.

But the Chinese car companies started to hit their stride shortly after 2019. This is when Tesla, flush with the success of its battery cars, built a factory in Shanghai. This may have been a strategic error, as it seemed to provide the impetus, as well as a best-in-class example, for how the Chinese carmakers should proceed. Encouraged or even perhaps ordered by Chinese President Xi Jinping, the resultant Chinese car industry (BYD, of course, but also Chery, Great Wall, SAIC and a number of others) is now beating the door down to supplant US, Japanese, German and Korean carmakers with a slew of well-executed and inexpensive EV’s that feature superior battery life and a host of options as standard.

Meanwhile carmakers everywhere are increasingly dependent on Chinese technology

In Europe, Chinese battery manufacturers have rapidly gained market share, rising from under 10% in 2020 to approximately 65% today. This surge has come largely at the expense of Korean battery makers and local suppliers, including Northvolt, which filed for bankruptcy in March 2025.

Contemporary Amperex Technology Co. Ltd. (CATL) has been a key driver of this shift, growing its European market share from zero in 2019 to 45% currently. The company continues to scale its local manufacturing footprint, most recently announcing its third European plant, a joint venture with Stellantis in Zaragoza, Spain in December 2024.

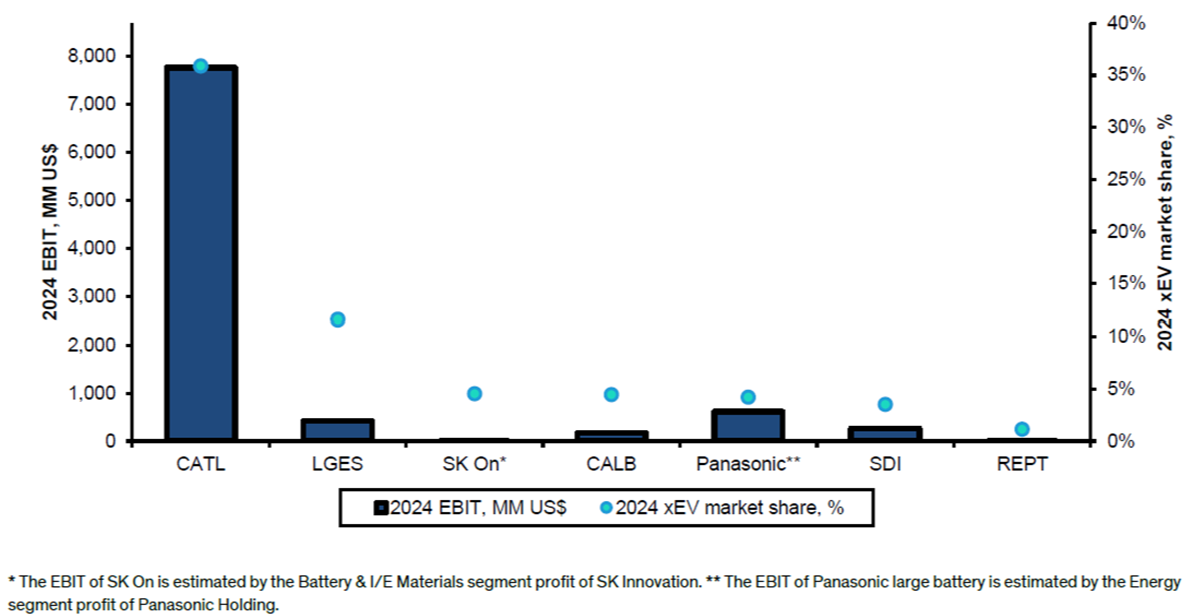

CATL holds a 37% share of the global battery market, including 42% in China, 39% in Europe, 13% in the United States, and 30% across other regions. Its customer base includes most major automotive companies, such as Tesla, Ford, Volkswagen, BMW, Mercedes-Benz, Toyota, Hyundai, Kia, Geely, XPeng, and Li Auto. The company’s competitive advantage is underpinned by its technology leadership—offering batteries with the highest energy density, fastest charging speeds, and industry-leading quality with the lowest return rates.

Due to its dominant position, CATL commands the vast majority of profits in the battery industry

Source: Bloomberg and Bernstein Analysis

These observations underpin investments into BYD and CATL

These investments come after a number of years in which there was no investment in Chinese companies. Part of the absence has been due to weak underlying investment cases. Another issue has been the risk of over-regulation on the part of the Chinese state itself. This risk seems to have eased this year (at least for this industry regarded as strategic to the government).

The decision to re-enter China in a risk-controlled way highlights that investing today calls for a flexible approach in which returns can be realistically judged to be in sight. It contrasts with, say, quantum computing which, while important, does not yet meet the criteria for inclusion in the portfolio.

Lastly, it is worth calling out the return for the year ending 30 June 2025, with the Fund returning +21.7%, net-of-fees with outperformance of +3.7%.relative to the MSCI All Countries World Index (net) (as expressed in AUD from Bloomberg). This return was achieved by muting the noise created by short-term news drivers such as tariffs, so as to better focus on long-term value creation.

Share this Post