Source: ChatGPT

Until now, the largest IPO ever (by funds subscribed) was Saudi Aramco, which in 2019 raised ~US$26 billion at a valuation of US$1.7 trillion. This also made it the largest company at the time (that many disruptors have since surpassed its value shouldn’t be a surprise…)

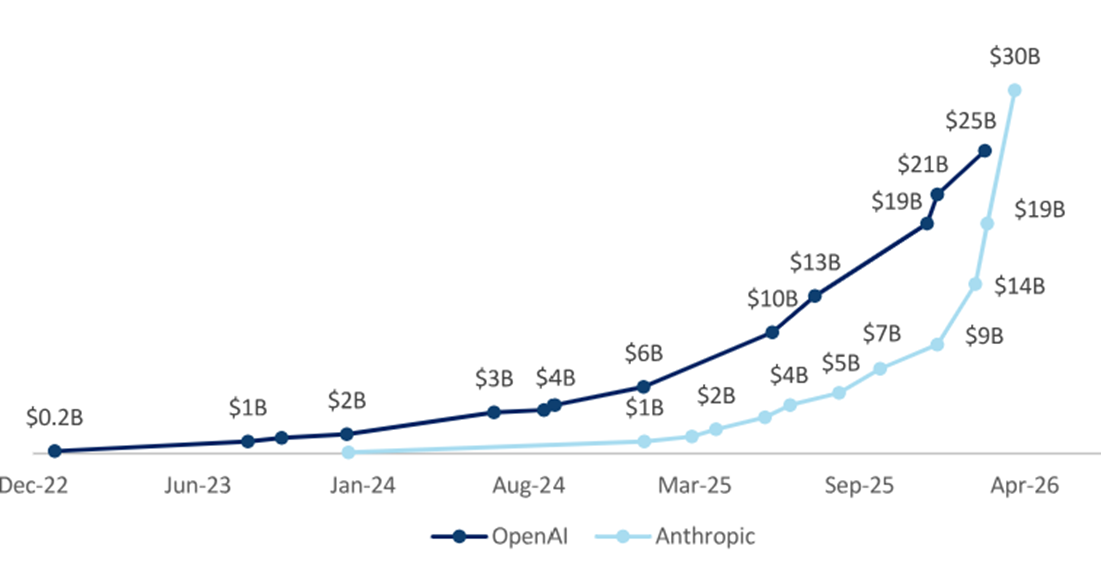

As we covered back in January, OpenAI (maker of ChatGPT) raised over US$100bn at a valuation of US$830bn to fund its AI infrastructure buildout. At the time this seemed excessive, but given subsequent news about OpenAI reaching almost US$30bn in Annual Recurring Revenue (ARR) and Anthropic actually surpassing OpenAI (tripling ARR in a few short months), it seemed a prudent decision. Anthropic (maker of Claude) subsequently raised US$30bn at a valuation of US$380bn.

ARR of Anthropic and OpenAI

And now riding two of the hottest trends of the moment (Artificial Intelligence and Space), it seems OpenAI, Anthropic and SpaceX are coming to a public market near you.

But the key question is: what are you paying for?

Out-of-this-world valuations

Reporting suggests OpenAI is looking to come to market at a valuation of US$1T+. Anthropic isn’t far behind, with more recent discussions suggesting its valuation could be upwards of $600bn.

As has been reported widely, both companies are burning through a lot of cash. US technology journal “The Information” reported that OpenAI anticipates it will chew through US$200bn over the next four years, while Anthropic is expecting a more meager deficit of US$25bn (although Anthropic’s estimates were made earlier this year, which is geological time for AI). The burn rate may now be worse as a result of the shift from reasoning models, ie “give me an answer about this”, to much more compute-intensive agentic workloads, “do this entire task for me.” This has led both companies to make significant commitments for additional compute capacity with major hyperscalers and leading semiconductor companies.

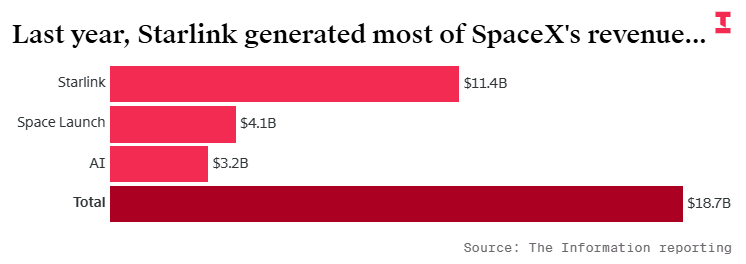

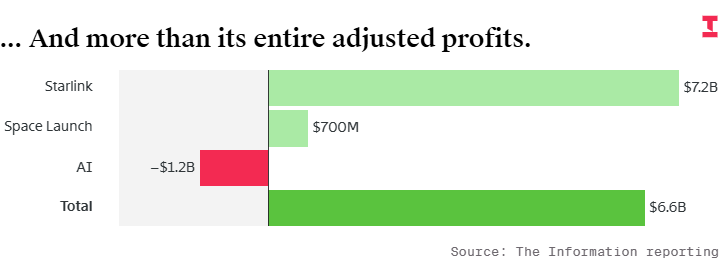

Meanwhile, SpaceX is planning to raise US$75bn at a valuation of US$2T (three times the size of Saudi Aramco’s IPO funds subscribed). It is worth recalling that SpaceX officially merged with xAI in February 2026 (which had previously subsumed Twitter/X in March 2025).

SpaceX brought back to earth by expensive AI efforts

Preliminary financials reported by “The Information” suggest a very solid satellite/internet business, with US$11.4bn in revenue and EBITDA margins of ~70% – but a cash burning AI business that’s only likely to get worse (similar to OpenAI and Anthropic).

While acknowledging that these figures are a point in time and don’t show how growth is trending, a US$2T price tag suggests that the company is being valued at > 100x revenue or > 300x EBITDA. This compares to OpenAI and Anthropic at a much more ‘digestible’ ~30x and ~20x revenue, respectively.

Would Loftus Peak participate in these IPOs?

We are often asked if we’ll be investing in these companies when they come to market. The simple answer is that it will depend on the financial health of these companies. Despite the significant media coverage and the trickle of cherry-picked financials (like above), there is no definitive public information about these companies.

Within Loftus Peak’s framework, if the valuations stack up, these companies would fall into the smaller part of the portfolio where allocations are relatively ‘riskier’ – i.e. companies with significant top line growth, but a lack of profitability and significant cashburn. We are also already indirectly exposed to these companies through the portfolio’s investments in semiconductor companies (or what refer to as the ‘tools’) and hyperscalers (‘enablers’). This is our present choice as an active manager.

But whether you like it or not, you might end up with direct exposure if you use passive funds.

Passive indices forced to get active

As a result of the unprecedented size of these IPOs, the indices that passive funds track are looking to bend the rules to include these companies sooner than usual.

For example, the Nasdaq Stock Exchange is proposing that the amount of time a company has to be listed before being included in the Nasdaq-100 (the 100 largest non-financial companies listed on the Nasdaq stock exchange) be reduced from 90 days to 15 days (if the company ranks within the top 40).

In addition to market capitalisation and other requirements, the S&P500 requires its constituents to have been GAAP profitable in the most recent quarter and for the trailing four quarters in aggregate. Given media reports it’s highly unlikely any of these companies are GAAP profitable.

Buy high, sell low?

An example of the potential downsides to passive strategies was highlighted by the AFR when out-of-favour Australian technology company Atlassian fell out of the Nasdaq-100 and was replaced by Sandisk. Sandisk makes memory components for smartphones and PCs, but also datacentres. As a result of AI, memory pricing has increased dramatically (higher smartphone and PC prices will be collateral damage). Sandisk was spun out of another company just over a year ago and has risen +2,800% since then (not a typo). It is only after this run, that it is being added to the index.

Historically, memory has been a very cyclical industry with strong rallies as demand exceeds supply, but when that equation flips the corrections can be very severe (look at share price charts of Samsung, SK Hynix and Micron for reference). Passive investors should be conscious of their growing exposure to such companies. The index methodologies have the potential perverse outcome of entering (buying) these names at the top and exiting (selling) at the bottom: not a great strategy for investment returns.

The bottom line

OpenAI didn’t have a business model three years ago and Anthropic was founded just five years ago. SpaceX has been around for longer, and has a strong rocket / satellite business, but a massively unprofitable AI company attached to it. That isn’t to say that they can’t or won’t be good businesses, but that we are at the beginning of global AI integration and the range of future outcomes remains incredibly wide.

The pace of change has never felt so fast, and it’s moments like these that we believe active management is crucial. We are believers in AI and the eventual opportunity in space, but we are also firm believers in valuation. It is the combination of both our philosophy of disruption and strict valuation methodology that has generated return for clients to date.

We very much look forward to the IPOs of these companies, both to get a look under the hood but also welcome to public markets what are potentially the world’s next generation of disruptors.

Share this Post