Hold onto your SOX

Semiconductors have represented Loftus Peak’s single largest portfolio sub-industry for several years. Over the last seven weeks, this positioning has given us a front-row seat to arguably the most dramatic move the space has ever seen. The Philadelphia Semiconductor Index (SOX) has surged ~60% since March. Of course, Loftus Peak isn’t built to track a single industry; we actively balance our semiconductor exposure against other disruptive opportunities, guided by valuation.

But with some semiconductor stocks doubling and tripling, it begs the question: is there any more upside?

Context is key

Taking a step back, the SOX was flat for the five months between the end of October 2025 and March 2026. The excitement around a string of massive AI deals quickly turned to concern over sustainability, capex Return on Investment (ROI), and ‘circular’ financing, hastening many of the AI chip majors’ ascents.

Despite strong guidance, investors preferred to exit these names or instead target specific AI hardware ecosystem bottlenecks. So while large SOX weights like Nvidia traded down, smaller stocks traded up significantly. Bottlenecks became evident in solid state drives, hard disk drives and optical transceivers. These small stocks started doubling and tripling as massive AI demand introduced pricing power these companies had never seen before. Commodity DRAM (much of which is for smartphones/PCs) fell into structural shortage pushing memory companies’ share prices up ~50% during the five month period.

In the first few months of the year, the market had engaged in the so-called HALO trade as a hedge against AI disruption – moving to stocks with Heavy Assets and Low Obsolescence (see our latest video for more details). The Iran conflict unravelled this trade, as oil is a key cost input for the many companies that formed the HALO trade, leaving investors to look for secular growth at attractive valuations.

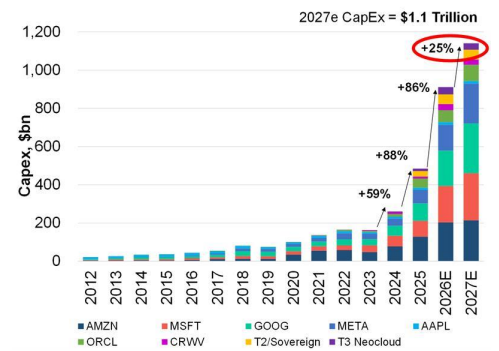

Semiconductors were the obvious answer and they only became more compelling as new data points emerged. Anthropic’s revenues scaled at an unprecedented pace, OpenAI/Anthropic successfully raised record levels of capital, hyperscalers accelerated revenue and increased their CapEx guidance for spending on AI cloud infrastructure (much of which goes towards semiconductors).

ARR of Anthropic and OpenAI

Source: Nanobanana

Source: Nanobanana

April’s CPU renaissance and memory boom

The shift towards agentic AI, AI that can complete tasks on its own, depends on the use of external connectors or applications. These cannot be completed by the GPUs that power the actual intelligence of AI. Instead the less powerful, more flexible CPUs execute these tasks after the GPU interprets user requests and plans the agentic workflow. This dynamic drives demand for a new CPU-specific rack for deployment next to the GPU racks. Accordingly, at earnings, AMD raised their 2030 server TAM from the 60bn announced in November to USD 120bn – a doubling in just over six months! Analysts at brokers like Evercore already estimate a USD 223bn TAM for CPUs in 2030. Unlike some of the smaller chip names, Intel and AMD (the two main CPU players) already had a combined market cap of over USD a little over USD 0.5tn at the end of March. They are now over USD 1.3tn.

Samsung, Micron and SK Hynix represented a combined market cap of almost USD 1.5tn and had performed strongly over the previous 6 months. Since then, their combined value is around USD 3.0tn with Samsung becoming the second Asian companies to cross the USD 1 trillion in market cap threshold (after TSMC). The price for commodity DRAM has risen meteorically due to AI and this pushes the earnings leverage of these companies through the roof. According to KB Securities, Samsung may be the most profitable company in the world next year.

There ARE pockets of euphoria…

ARM licenses CPU architecture for royalties, but its core smartphone revenue faces cyclical macro headwinds and rising memory costs. While its datacentre presence grows through custom AI chips, ARM’s near term outlook remains under pressure. Nevertheless, the stock has traded up to a significant valuation premium against peers.

Valuations also seem stretched for analog semiconductor companies (those that sell into industrials and automotives). Despite re-rating significantly, these names remain macro-dependent with a weak consumer outlook. While names like ON and IFX benefit from margin-boosting inventory builds, it is unclear if this restocking is durable or merely a hedge against supply chain disruptions in Hormuz. Unlike optical transceivers or HDD, their datacentre exposure is less specialized and unlikely to face AI-driven shortages.

Navigating the rate of change in valuations

This is not our first rodeo. With over a decade spent monitoring the semiconductor tools driving AI, we are seasoned in this space. We are long-term believers in AI-driven disruption but valuation remains the critical factor. While aggregate semiconductor valuations are not excessively stretched, this is not true for each and every stock.

Our goal is to provide clients with the most favourable risk-to-reward opportunities within disruption, and we believe there is still valuation support within semiconductor tools that enable AI. Now, as the share prices, valuations and outlooks for these companies are changing at an almost daily pace, we believe that discipline and understanding is more indispensable than ever.

Share this Post